When students first approach U.S. taxation, it often appears complex and layered. However, once the foundational structure is understood, the system becomes much more logical and interesting. Let’s break it down into simple, conceptual elements.

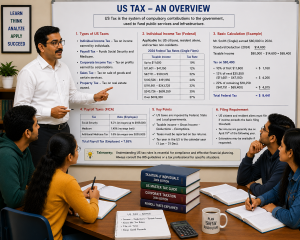

Unlike many countries, the United States follows a multi-level taxation system, where taxes are imposed at different levels:

- Federal Tax – Levied by the central government

- State Tax – Each state has its own tax rules (some states have no income tax)

- Local/City Tax – Certain cities or municipalities also impose taxes

This means a taxpayer may have to comply with multiple tax jurisdictions simultaneously, making compliance and planning more important.

Taxpayers need to file separate Federal, State and Local tax returns if applicable. Furthermore, each state has its own filing thresholds for individuals living and/or working in the states.

Taxes may be imposed on individuals (natural persons), business, partnerships, corporations, estates, trusts, or other forms of organization.

The United States uses a progressive tax system which means higher the income, the more taxes must be paid.

Taxes are levied on income, payroll, property, sales, capital gains, dividends, estates and gifts, as well as various fees.

Internal Revenue Service (IRS) is the tax authority in the US. – Federal tax returns are submitted/filed with the IRS. IRS comes under the Department of Treasury which is headed by the Secretary of the Treasury.

Tax Identification Numbers (TINs)

For tax filing and compliance, identification numbers are essential:

| SSN (Social Security Number) |

| Issued to U.S. citizens and residents |

| Used for employment and tax purposes |

| EIN (Employer Identification Number) |

| Used by businesses, partnerships, and corporations |

| ITIN (Individual Taxpayer Identification Number) |

| Issued to non-residents or individuals not eligible for SSN |

These numbers ensure proper tracking of tax obligations and filings.

Every taxpayer (individuals, business entities, etc.) must figure taxable income for an annual accounting period called a tax year. Each taxpayer must use a consistent accounting method, which is a set of rules for determining when to report income and expenses.

- Calendar Year – 12 consecutive months beginning January 1 and ending December 31.

- Fiscal Year – A fiscal year is 12 consecutive months ending on the last day of any month except December 31st.

- Short Tax Year – A short tax year is a tax year of less than 12 months. It occurs when

business start-up or close, change in accounting period

One of the most critical concepts in U.S. taxation is tax residency, which determines:

- Whether global income is taxable

- Whether only U.S.-source income is taxable

The commonly applied test is the Substantial Presence Test (SPT), which considers:

- Number of days stayed in the U.S.

- Presence over a 3-year period

Key Concept:

- Resident taxpayers → Taxed on worldwide income

- Non-resident taxpayers → Taxed only on U.S.-source income

In the U.S., different types of taxpayers file different forms. Let’s explore them.

- Form 1040 – Individuals

Used by:

- U.S. citizens

- Resident individuals

- Form 1040NR – Non-Residents

Key difference:

- 1040 → Global income

- 1040NR → Only U.S.-source income

- Form 1065 – Partnership Firms

They file Form 1065, but:

- No tax is paid at firm level

- Income is passed to partners

- Form 1120 – Corporations (C-Corp)

A regular corporation files Form 1120.

- Separate legal entity

- Pay tax at corporate level

Double taxation — company pays tax + shareholders pay on dividends.

- Form 1120S – S Corporations

S Corporations file Form 1120S

- Like partnership taxation

- Income passes through to shareholders

- From 1041

Trusts & Estates – think beyond individuals and companies—trusts or estates

Used for:

- Trust income

- Estate income

Now, let’s take a high-level view of the key tax forms, along with their original due dates, extended due dates, and the relevant extension forms.

Comparison Table (with Due Dates & Extension Forms)

| Form | Applicable To | Original Due Date* | Extended Due Date | Extension Form |

| 1040 | Individuals (Residents) | April 15 | October 15 | Form 4868 |

| 1040NR | Non-resident individuals | April 15 / June 15 | October 15 / December 15 | Form 4868 |

| 1065 | Partnerships | March 15 | September 15 | Form 7004 |

| 1120 | C-Corporations | April 15 | October 15 | Form 7004 |

| 1120S | S-Corporations | March 15 | September 15 | Form 7004 |

| 1041 | Trusts & Estates | April 15 | September 30 | Form 7004 |

Very Interesting.

Thank you!

Thank you.

Nicely Explained.

Thank you! Stay tuned….

Thank you. Stay tuned..

My first knowledge of US tax begins here that too in my way of understanding. Thank you so much sir. I request you to write one blog of US tax with respect to Indian tax.

I am thrilled to hear it!!