Financial statements are prepared according to a framework of accounting principles commonly known as GAAP (Generally Accepted Accounting Principles). GAAP includes accounting concepts, conventions, standards and disclosure requirements that guide companies in preparing financial statements in a consistent and comparable manner.

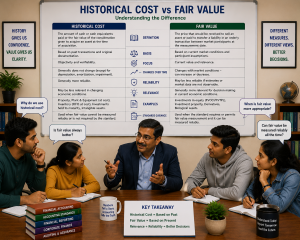

Traditionally, Indian Accounting Standards (AS) largely emphasized the historical cost concept, under which assets were generally recorded at original purchase price less depreciation. However, with globalization and increasing participation of international investors, financial reporting gradually moved towards Ind AS and IFRS-oriented reporting frameworks, where fair value measurement became increasingly important for certain classes of assets and financial instruments.

As a result, the same asset may appear at significantly different values depending upon whether historical cost accounting or fair value accounting is followed. The following case study helps us practically understand this important transition from traditional AS-based reporting to Ind AS-oriented fair value reporting.

Case Study: Historical Cost under AS vs Fair Value under Ind AS

Liston Company Ltd. is a technology company engaged in supporting software services and infrastructure development. In 2015, the company purchased an office building in Bengaluru for its corporate operations. Over the years, rapid commercial development in the area significantly increased the market value of the property.

This example helps students understand how the same asset may appear differently under traditional Accounting Standards (AS) and under the fair value-oriented Ind AS framework.

Background information

| Particulars | Amount (Rs) |

| Cost of Office Building purchased in 2015 | 2,00,00,000 |

| Accumulated Depreciation till 2026 | 20,00,000 |

| Fair Market Value in 2026 | 5,00,00,000 |

Scenario 1: Treatment under Traditional AS (Historical Cost Approach)

Under traditional Accounting Standards, assets are generally shown at:

- historical cost,

- less accumulated depreciation.

Therefore:

| Particulars | Amount (Rs.) |

| Original cost of Building | 2,00,00,000 |

| Less: Accumulated Depreciation | (20,00,000) |

| Carrying amount under AS | 1,80,00,000 |

Thus: Book Value under AS = Rs. 1.8 crore

Observation

Even though the market value became Rs.5 crore, the balance sheet under traditional AS continues showing the asset close to original cost.

This approach emphasizes:

- objectivity,

- reliability,

- actual transaction value.

Scenario 2: Treatment under Ind AS (Fair Value / Revaluation Approach)

Under Ind AS, companies may adopt fair value or revaluation approaches depending upon the applicable standard and accounting policy.

Suppose the company adopts revaluation model under Ind AS.

Then:

| Particulars | Amount (Rs) |

| Fair Market Value of Building | 5,00,00,000 |

| Carrying amount under Ind AS | 5,00,00,000 |

Therefore: Fair Value under Ind As = Rs. 5 crores.

Increase due to Revaluation

| Particulars | Amount (Rs) |

| Fair Value | 5,00,00,000 |

| Book Value under AS | 1,80,00,000 |

| Increase in Value | 3,20,00,000 |

Thus: Revaluation increase = Rs.3.2 crores

Relevant Standards

| Standard | Purpose |

| AS 10 | Property, Plant & Equipment (including depreciation principles after withdrawal of AS 6) |

| Ind AS 16 | Property, Plant & Equipment |

| Ind AS 113 | Fair Value Measurement |

Key points for understanding

This Rs.3.2 crore increase is generally:

- not treated as normal operating income,

- not shown as revenue from operations.

Under Ind AS 16, such revaluation increase is generally recognized through:

- Other Comprehensive Income (OCI),

- and accumulated under Revaluation Surplus within Equity.

Therefore, students must understand:

Comparative Understanding

| Basis | Traditional AS | Ind AS / IFRS-Oriented Approach |

| Asset Measurement | Historical Cost | Fair Value / Revaluation |

| Value Reported | Rs.1.8 crore | Rs.5 crore |

| Focus | Reliability | Current economic reality |

| Nature | Conservative | Market-oriented |

| Impact of Market Rise | Ignored until sale | May be recognized through OCI |

Very easy to understand

Thank you.