Professor: When we hear the term ‘U.S. Taxation,’ many students imagine a highly complex system full of forms and calculations. But if we understand the logic behind the system step-by-step, it becomes far more structured and interesting than it first appears

Professor:

Students, today we are not merely learning tax computation. We are learning the logical flow of a U.S. tax return.

Think of it like a pipeline:

- Income enters at the top

- Adjustments happen step-by-step

- Final output becomes either:

- Tax Refund

- Or Tax Due

Let’s understand each stage carefully.

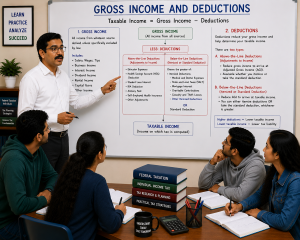

1. Gross Income

Professor:

What do you think “Gross Income” means?

Student:

Total income before deductions?

Professor:

Correct.

Gross income may include:

- Wage

- Interest income

- Dividend income

- Business income

- Rental income

- Capital gains

2. Less: Deductions or Adjustments to Income

These are called “Above-the-line deductions.”

Examples:

- Traditional IRA contribution

- Student loan interest

- Health Savings Account deduction

Professor:

Why do you think these are important?

Student:

Because they reduce income before tax calculation.

Professor:

Exactly.

3. Adjusted Gross Income (AGI)

After adjustments:

Why AGI is Important

AGI is one of the most important numbers in U.S. taxation because many:

- deductions,

- credits,

- and eligibility rules

depend on AGI.

4. Greater of: Standard Deduction or Itemized Deduction

Professor:

Now taxpayer gets another benefit.

Two options:

- Standard Deduction

- Itemized Deduction

The taxpayer usually chooses whichever is higher.

Standard Deduction

Fixed deduction allowed by law.

Example:

- Single filer

- Married filing jointly

Each category has prescribed amount.

Itemized Deduction (BLD)

Actual eligible expenses such as:

- Mortgage interest

- State taxes

- Charitable contributions

- Medical expenses (subject to rules)

These are called “Below-the-line deductions.”

5. Taxable Income

Now:

Professor: This is the income on which tax rates are applied.

6. Tax Rates ?

Professor:

Does the U.S. follow a flat tax system?

Student:

No, progressive tax system.

Professor:

Correct.

Higher income → Higher tax brackets.

7. Tax Before Credits & Payments

At this stage:

Taxable Income × Tax Rates=Tax Before Credits

8. Less: Tax Credits

Professor:

Now comes a very powerful concept.

- Deduction reduces income

- Credit reduces tax directly

Examples of Credits

- Child Tax Credit

- Education Credit

- Foreign Tax Credit

Important Concept

Refundable vs Non-Refundable Credits

Non-Refundable Credit

Can reduce tax only up to zero.

Refundable Credit

Even if tax becomes zero, excess may be refunded.

Example

Tax liability = $1,000

Refundable credit = $1,500

- Tax becomes zero

- Extra $500 refunded

9. Total Federal Tax Liability

After determining the taxable income, the applicable federal tax rates are applied to compute the Federal Income Tax.

The taxpayer may then reduce this tax through available tax credits.

In certain situations, additional federal taxes may also apply, such as:

- Self-Employment Tax (SECA) for self-employed individuals

- Alternative Minimum Tax (AMT)

- Net Investment Income Tax (NIIT)

- Additional Medicare Tax

- Other special federal taxes prescribed by law

Thus, the taxpayer’s Total Federal Tax Liability may be summarized as:

Federal Income Tax

Less: Tax Credits

Add: Additional Federal Taxes (if applicable)

= Total Federal Tax Liability

Insight

For employees, Social Security and Medicare taxes are generally collected through the payroll system under FICA (Federal Insurance Contributions Act) and are withheld from salary.

For self-employed individuals, the equivalent Social Security and Medicare taxes are paid through SECA (Self-Employment Contributions Act) and become part of the federal tax computation.

10. Less: Tax Payments and Refundable Credits

After computing the Total Federal Tax Liability, credit is given for taxes already paid during the year, including:

- Federal income tax withheld from salary

- Estimated tax payments

- Refundable tax credits

- Other eligible federal tax payments

These amounts represent advance payments made toward the taxpayer’s federal tax obligation.

11. Result: Tax Due or Refund

The final step is to compare the Total Federal Tax Liability with the payments and credits already available.

Total Federal Tax Liability

Less: Tax Payments and /Non-refundable/Refundable Credits

= Tax Due or Tax Refund

- If Total Federal Tax Liability exceeds payments and credits, the taxpayer must pay the balance as Tax Due.

- If payments and refundable credits exceed Total Federal Tax Liability, the taxpayer is entitled to a Tax Refund.

Summary FormulaTax Due (or Refund) = Total Federal Tax Liability − Tax Payments – Non-refundable/Refundable Credits

very easily explained sir 😊

Explained in a easy way for us students.

Thank you. Keep updated..

Sir , it will be very helpful if you give a blog regarding provisions for bad debt

noted. it will be coming soon.

Thank you so much for such valuable information and notes Sir.

These notes will really be our most valuable weapons in our journey.

Good and so glad this was helpful!!

Learning and growing with your blogs. Thank you sir.

Happy to know that you have found it helpful!!

Wonderful explanation sir

Keep following!!