Accounting is often described as the language of business. Yet, many students are introduced to accounting as a subject of rules, formats, journal entries and calculations. As a result, they sometimes learn the mechanics of accounting without understanding the logic behind it.

Accounting is a systematic process of identifying, recording, classifying, summarizing and communicating financial information. Before an accountant record anything, an important question must be answered: what exactly should be recorded?

Step 1: Event vs Transaction

Professor: Tell me, if a customer visits a shop and asks for the price of a laptop, should it be recorded in the books?

Student A: No, because no sale has taken place.

Professor: Correct.

This is an event, but not an accounting transaction. An event is any occurrence relating to the business.

Now suppose the customer purchases the laptop for Rs.50,000.

Student B: Then it becomes a transaction because money is involved.

Professor: Exactly.

Simple Distinction

| Item | Meaning |

| Event | Any occurrence relating to the business |

| Transaction | An event having a measurable financial impact |

Thus, every transaction is an event, but every event is not a transaction.

Step 2: Why do we need debit and credit?

The need for debit and credit arises from the Dual Aspect Concept.

Professor: Let’s understand this learning flow to answer the above question

Event→Transaction→Journal→Ledger→Trial Balance→Financial Statements

Student C: Sir, before learning journal entries, what do Debit and Credit mean?

Teacher: Excellent question.

Many beginners think:

- Debit means receiving.

- Credit means giving.

However, in accounting, debit and credit are simply the two sides of recording a transaction.

Step 3: Dual Aspect Concept

The Dual Aspect Concept states:

“Every accounting transaction has at least two effects.”

For example:

The owner invests Rs.1,00,000 in the business.

What happens?

- Cash increases.

- Capital increases.

One transaction, two effects.

This principle forms the foundation of the double-entry system of accounting.

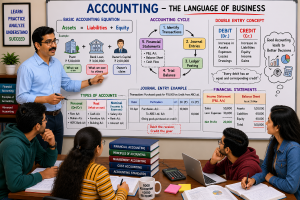

Step 4: Understanding Debit and Credit through the Accounting Equation

The basic accounting equation is:

Assets = Liabilities + Capital

A more comprehensive version is:

Assets = Liabilities + Capital + Income – Expenses

To keep this equation balanced, accountants use debit and credit.

Basic Rules

| Account Category | Increase | Decrease |

| Assets | Debit | Credit |

| Liabilities | Credit | Debit |

| Capital / Equity | Credit | Debit |

| Income | Credit | Debit |

| Expenses | Debit | Credit |

Example

Business pays salary of Rs.5,000.

- Salary expense increases → Debit

- Cash decreases → Credit

Journal Entry:

Salary A/c Dr. Rs 5,000

To Cash A/c Rs.5,000

Step 5: Recording Transactions in the Journal

Student A: Sir, once we know debit and credit, where do we record transactions?

Professor: In the Journal.

The Journal is called the Book of Original Entry because transactions are first recorded here.

Example

Purchased goods for cash Rs.10,000.

Journal Entry:

Purchases A/c Dr. Rs.10,000

To Cash A/c Rs.10,000

The Journal records transactions in chronological order.

Step 6: Posting to the Ledger

Student B: Why is the Journal not enough?

Professor: Because the Journal tells us what happened, but it does not tell us the balance of each account.

For this purpose, transactions are transferred to the Ledger.

The Ledger is known as the Principal Book of Accounts.

For example:

- All cash transactions are accumulated in the Cash Account.

- All purchase transactions are accumulated in the Purchases Account.

The Ledger helps us determine the balance of each account.

Step 7: Preparing the Trial Balance

Student C: What happens after the Ledger?

Professor: We prepare a Trial Balance.

A Trial Balance is a statement showing the debit and credit balances of all ledger accounts.

Its primary purpose is to check the arithmetical accuracy of the books of accounts.

If total debits equal total credits, the books are said to be arithmetically correct.

Step 8: Financial Statements

Student D: Does accounting end with the Trial Balance?

Professor: No.

The Trial Balance serves as the basis for preparing financial statements such as:

- Statement of Profit and Loss

- Balance Sheet

- Cash Flow Statement

These statements communicate financial information to:

- Owners

- Investors

- Lenders

- Government authorities

- Other stakeholders

Key Takeaway

Accounting is not merely a collection of rules, journal entries and calculations. It is a logical process that begins with identifying financial transactions and ends with communicating useful information to decision-makers. The concepts of debit and credit, the dual aspect concept, the accounting equation, the journal, the ledger and the trial balance are all interconnected parts of a single accounting system designed to present a reliable picture of a business’s financial position and performance.

This module added a new perspective to my understanding of finance. Thank you for creating such a content that is not only informative but also practical and easy to grasp. Truly appreciate my finance mentor and the course content!

Diya – Thank you! I am pleased to know that the content met your needs.