Accounting is often referred to as the language of business, but every language has its own grammar and rules. Similarly, the entire accounting system is built upon a few fundamental principles that ensure every business transaction is recorded accurately and systematically. Among these, the concepts of debit and credit, the Golden Rules of Accounting, the Dual Aspect Concept, and the Accounting Equation occupy a central position.

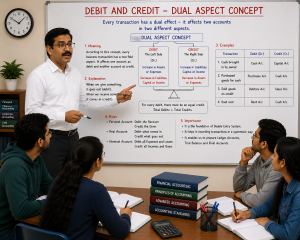

Whenever a business transaction occurs, it affects at least two accounts. This principle, known as the Dual Aspect Concept, forms the foundation of the double-entry system of accounting. The mechanism for recording these dual effects is provided through the concepts of debit and credit, while the Golden Rules of Accounting guide us in determining which account should be debited and which should be credited.

The cumulative effect of all such transactions is reflected through the Accounting Equation, which establishes the relationship between a business’s assets, liabilities, and owner’s equity. In fact, the accounting equation is the mathematical expression of the dual aspect concept and ultimately forms the basis of the Balance Sheet.

Therefore, a clear understanding of debit and credit, the golden rules, the dual aspect concept, and the accounting equation is essential for every student of accounting. The following discussion and illustrations will demonstrate how these concepts are interconnected and together form the backbone of the accounting system.

Accounting Equation: Assets= Liabilities + Capital

Every transaction affects this equation.

Golden Rules of Accounting

Example 1

| Account Type | Represents |

| Personal Account | Persons, firms, companies, banks and institutions |

| Real Account | Tangible and intangible assets owned by the business |

| Nominal Account | Expenses, losses, incomes and gains of the business |

Example 2

| Account type | Golden rule | Example of accounts |

| Personal Account | Debit the receiver, Credit the giver | Debtors A/c, Creditors A/c, Capital A/c, Bank A/c, Ram A/c, SBI A/c |

| Real Account | Debit what comes in, Credit what goes out | Cash A/c, Furniture A/c, Machinery A/c, Building A/c, Inventory/Stock A/c, Land A/c |

| Nominal Account | Debit expenses/losses, Credit incomes/gains | Salary A/c, Rent A/c, Interest paid A/c, Commission received A/c, Sales A/c, Discount received A/c |

These rules guide:

- which account should be debited,

- which account should be credited.

Important conceptual link

- The accounting equation explains why accounting remains mathematically balanced.

- The golden rules explain how transactions are recorded through debit and credit.

Thus:

- Accounting Equation = theoretical foundation

- Golden Rules = practical recording mechanism

Let us understand how every transaction simultaneously leads into:

- Dual Aspect Concept

- Debit and Credit

- Golden Rules of Accounting

- Accounting Equation

Example 1-Suppose Selva Company purchases machinery for cash Rs.1,00,000

Golden Rule

Machinery A/c → Real Account

Cash A/c → Real Account

Golden Rule:

- Debit what comes in → Machinery Dr.

- Credit what goes out → Cash Cr.

Journal Entry:

| Particulars | Dr. | Cr. |

| Machinery A/c Dr. | 1,00,000 | |

| To Cash A/c | 1,00,000 |

Accounting Equation

| Effect | Impact |

| Machinery increases | Asset increases |

| Cash decreases | Asset decreases |

Net effect:

- total assets remain same,

- equation remains balanced.

Example 2

Owner introduces capital Rs.5,00,000 in cash.

Golden Rule application

Cash comes in → Debit Cash

Owner gives capital → Credit Capital

Journal Entry:

| Particulars | Dr. | Cr. |

| Cash A/c Dr. | 5,00,000 | |

| To Capital A/c | 5,00,000 |

Accounting Equation effect

| Assets | Liabilities + Capital |

| Cash +5,00,000 | Capital +5,00,000 |

Equation balances automatically.

Conceptual understanding

Every debit and credit ultimately changes the accounting equation

Thus:

- double entry system,

- golden rules,

- and accounting equation

are all interconnected parts of the same accounting framework.

The practical examples make it incredibly easy to see how the Dual Aspect Concept impacts the Accounting Equation in real-time. A great quick-reference guide for accounting basics.

good to hear that this content met your needs! Stay tuned..

Good… happy to know that it is useful for your understanding…