Prelude

In our previous blogs, we learned how business transactions are recorded in the Journal, classified in the Ledger and summarized in a Trial Balance.

A Trial Balance, however, is not the destination of accounting. It is merely a gateway to the preparation of financial statements.

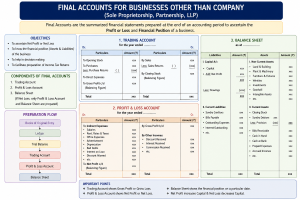

For a non-corporate entity such as a sole proprietorship or partnership firm, accountants traditionally prepare:

- Trading Account

- Profit & Loss Account

- Balance Sheet

On the other hand, corporate entities prepare financial statements in accordance with Schedule III of the Companies Act, 2013.

Before studying corporate financial statements, it is useful to understand the traditional approach because it clearly explains how profit is calculated and how assets and liabilities are presented.

What happens after the Trial Balance?

Professor: Students, after preparing a Trial Balance, what is the next step?

Student: Sir, financial statements?

Professor: Correct. But before preparing the Balance Sheet, we first determine profit.

This is done in some stages:

Stage 1: Trading Account

Stage 2: Profit & Loss Account

Stage 3: Profit & Loss Appropriation Account (Partnership Business)

Stage 4: Balance Sheet

Stage 1: Trading Account

Purpose

To determine:

Gross Profit or Gross Loss: arising from the core trading activities of the business.

What goes into the Trading Account?

Direct Expenses (Examples)

Opening Stock, Purchases, Direct Wages, Carriage Inward, Freight Inward, Manufacturing Expenses, Factory Power & Fuel.

Direct Incomes (Examples)

Sales, Closing Stock, Manufacturing income directly arising from trading or production activities.

Trading Account Example

| Particulars | Amount (Rs.) | Particulars | Amount (Rs.) |

| Opening Stock | 50,000 | Sales | 3,20,000 |

| Purchases | 2,00,000 | Closing Stock | 60,000 |

| Carriage Inward | 10,000 | ||

| Gross Profit c/d | 1,20,000 | ||

| Total | 3,80,000 | Total | 3,80,000 |

Stage 2: Profit & Loss Account

Purpose

To determine: Net Profit or Net Loss of the business.

What goes into the Profit & Loss Account?

Indirect Expenses

These are expenses incurred for administration, selling, distribution and financing activities.

Salary, Rent, Office Expenses, Insurance, Depreciation, Advertising, Audit Fees, Bank Charges and Interest on Loans.

Indirect Incomes

These are incomes not directly related to buying, manufacturing or selling goods.

Commission Received, Interest Received, Rent Received, Discount Received and Dividend Received, Profit on Sale of Assets etc.

Profit & Loss Account Example

Assume:

Gross Profit = Rs.1,20,000

| Particulars | Amount (Rs.) | Particulars | Amount (Rs.) |

| Salary | 30,000 | Gross Profit b/d | 1,20,000 |

| Rent | 15,000 | Commission Received | 10,000 |

| Depreciation | 5,000 | ||

| Net Profit | 80,000 | ||

| Total | 1,30,000 | Total | 1,30,000 |

Stage 3: Profit & Loss Appropriation Account (Partnership Firms)

Purpose

To distribute the Divisible Profit among partners after deducting some expenses according to the partnership deed.

Important Concept

Professor: Students, remember:

Profit & Loss Account determines profit.

Profit & Loss Appropriation Account distributes profit.

Therefore, Partner’s Salary, Interest on Capital and Partner’s Commission are not ordinary business expenses; they are appropriations (distributions) of profit among the partners.

Example:

Net Profit = Rs.1,00,000. The Partnership Deed provides for Interest on Capital Rs.10,000, Partner’s Salary Rs.20,000, and the remaining profit to be shared equally (assumed) between the partners.

Profit & Loss Appropriation Account

| Particulars | Amount (Rs.) | Particulars | Amount (Rs.) |

| Interest on Capital | 10,000 | Net Profit b/d | 1,00,000 |

| Partner’s Salary | 20,000 | ||

| Share of Profit – Partner A | 35,000 | ||

| Share of Profit – Partner B | 35,000 | ||

| Total | 1,00,000 | Total | 1,00,000 |

Stage 4: Balance Sheet

Purpose

To show the financial position of the business on a particular date.

Examples of Assets: Cash, Bank Balance, Debtors, Inventory, Furniture and Machinery.

Examples of Liabilities: Creditors, Loans and Outstanding Expenses.

Capital

- Capital

- Net Profit/Divisible profit

− Drawings

(In a partnership, after considering appropriations.)

Understanding Additional Adjustments

One of the most important areas in accounting is year-end adjustments.

Most adjustments have two effects, reflecting the Dual Aspect Concept.

Common Year-End Adjustments and Their Dual Effects

| Adjustment | First Effect | Second Effect |

| Closing Stock | Credited to Trading Account | Shown as a Current Asset in the Balance Sheet |

| Outstanding Salary | Added to Salary Expense in Profit & Loss Account | Shown as a Current Liability in the Balance Sheet |

| Depreciation | Debited to Profit & Loss Account | Reduces the value of the related Asset in the Balance Sheet |

| Prepaid Insurance | Reduces Insurance Expense in Profit & Loss Account | Shown as a Current Asset in the Balance Sheet |

| Accrued Income | Credited Profit & Loss Account | Shown as a Current Asset in the Balance Sheet |

| Unearned Income (Income Received in Advance) | Reduced Income in Profit & Loss Account | Shown as a Current Liability in the Balance Sheet |

Memory Table

| Adjustment | Category | First Effect | Second Effect |

| Closing Stock | Trading A/c + Balance Sheet | Credited to Trading A/c | Current Asset |

| Outstanding Salary | P&L A/c + Balance Sheet | Added to Salary Expense | Current Liability |

| Depreciation | P&L A/c + Balance Sheet | Debited to P&L | Reduces Asset Value |

| Accrued Income | P&L A/c + Balance Sheet | Credited to P&L | Current Asset |

Takeaway

Sole Proprietorship

Trial Balance → Trading Account → Gross Profit → Profit & Loss Account → Net Profit → Balance Sheet

Partnership Firm

Trial Balance → Trading Account → Gross Profit → Profit & Loss Account → Net Profit → Profit & Loss Appropriation Account → Divisible Profit→ Balance Sheet