Imagine that a business records hundreds of transactions every month. While the Journal records transactions in chronological order, it does not tell us the total cash available, the amount owed by customers, or the amount payable to suppliers.

To obtain this information, accountants classify journal entries into separate accounts known as Ledgers. Once the balances of all ledger accounts are determined, they are summarized in a Trial Balance, which serves as the foundation for preparing financial statements.

Let us understand this process

What is a Ledger?

Professor: Students, suppose a business records the following transactions:

- Owner introduces capital Rs.1,00,000 in bank.

- Purchased goods on credit Rs.40,000.

- Sold goods on credit Rs.60,000.

- Paid rent Rs.10,000 through bank.

All these transactions have been recorded in the Journal.

Now tell me, how can we find:

- Total bank balance?

- Amount receivable from customers?

- Amount payable to suppliers?

Student A: Sir, we need separate records for each account.

Professor: Exactly.

That is the purpose of a Ledger.

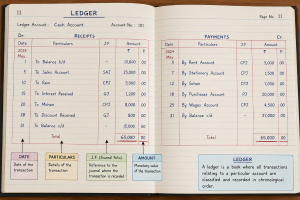

Definition

A Ledger is the principal book of accounts in which transactions relating to a particular account are accumulated and classified.

Why is a Ledger necessary?

The Journal tells us: What happened and when it happened.

The Ledger tells us: The balance of each account.

Types of Ledgers

1. Personal Ledger

Contains accounts relating to persons and organizations.

Examples: Customers, Suppliers, Debtors and Creditors.

Example: Raj A/c, ABC Suppliers A/c, TSS Ltd.

2. Real Ledger

Contains accounts relating to assets.

Examples: Cash A/c, Bank A/c, Furniture A/c, Machinery A/c and Building A/c.

3. Nominal Ledger

Contains accounts relating to income, expenses, gains and losses.

Examples: Salary A/c, Rent A/c, Commission A/c, Interest Income A/c and Sales A/c.

From Journal to Ledger

Professor: Let us post the transactions into ledger accounts.

Journal Entries

- Bank A/c Dr. Rs.1,00,000

To Capital A/c Rs.1,00,000 - Purchases A/c Dr. Rs.40,000

To ABC Suppliers A/c Rs.40,000 - Raj A/c Dr. Rs.60,000

To Sales A/c Rs.60,000 - Rent A/c Dr. Rs.10,000

To Bank A/c Rs.10,000

Ledger Balances

After posting, the balances may appear as follows:

| Ledger Account | Balance Type | Amount (Rs.) |

| Bank A/c | Debit | 90,000 |

| Purchases A/c | Debit | 40,000 |

| Raj (Customer) A/c | Debit | 60,000 |

| Rent A/c | Debit | 10,000 |

| ABC Suppliers A/c | Credit | 40,000 |

| Capital A/c | Credit | 1,00,000 |

| Sales A/c | Credit | 60,000 |

What is a Trial Balance?

Student B: Sir, what do we do with these balances?

Professor: We prepare a Trial Balance.

Definition

A Trial Balance is a statement prepared by listing the balances of all ledger accounts on a particular date to verify the arithmetical accuracy of the books of accounts.

Using the ledger balances above:

| Account Name | Debit Rs.) | Credit (Rs.) |

| Bank A/c | 90,000 | – |

| Purchases A/c | 40,000 | – |

| Raj A/c | 60,000 | – |

| Rent A/c | 10,000 | – |

| ABC Suppliers A/c | – | 40,000 |

| Capital A/c | – | 1,00,000 |

| Sales A/c | – | 60,000 |

| Total | 2,00,000 | 2,00,000 |

Why do debit and credit totals match?

Student C: Sir, why are both totals equal?

Professor: Because every transaction is recorded using the Double Entry System.

Every debit has corresponding credit.

Therefore:

Total Debits = Total Credits

Why do debit and credit totals match?

Student C: Sir, why are both totals equal?

Professor: Because every transaction is recorded using the Double Entry System.

Every debit has corresponding credit.

Therefore:

Total Debits = Total Credits

Does a balanced Trial Balance mean no errors?

Student D: If the Trial Balance agrees, are the books completely correct?

Professor: Not necessarily.

A Trial Balance confirms only the arithmetical accuracy of postings.

Certain errors may still exist, such as:

- Complete omission of a transaction.

- Recording a transaction in the wrong account.

- Errors of principle.

Connection with Financial Statements

Once the Trial Balance is prepared:

- Income and expense accounts are used to prepare the Statement of Profit and Loss.

- Asset, liability and capital accounts are used to prepare the Balance Sheet.

After the Trial Balance table, check this simple observation:

| Type of Account | Usually appears in Trial Balance As |

| Assets | Debit Balance |

| Expenses | Debit Balance |

| Liabilities | Credit Balance |

| Capital | Credit Balance |

| Income | Credit Balance |