One of the most critical concepts in U.S. taxation is tax residency, because it determines the scope of taxable income:

- Whether global income is taxable or

- only U.S.-source income is taxable

In simple terms:

- Resident → Taxed on worldwide income

- Non-resident → Taxed only on U.S.-source income

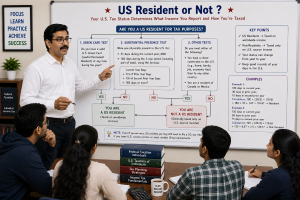

U.S. Tax Residency Decision Flowchart

Step 1: Citizenship Test

Are you a U.S. Citizen?

- YES → Resident for tax purposes (Worldwide income taxable)

- NO → Go to Step 2

Step 2: Green Card Test

Do you hold a valid Green Card at any time during the year?

- YES → Resident for tax purposes

- NO → Go to Step 3

Step 3: Exempt Individual Check (Before SPT)

Are you an Exempt Individual?

- Student (F, J, M, Q visa – within 5 years)

- Teacher/Trainee (J, Q visa – within 2 of last 6 years)

- YES → Do NOT count days → non-resident (generally)

- NO → Go to Step 4

Step 4: Substantial Presence Test (SPT)

- 31 days during the current year, and

- 183 days during the 3-year period that includes the current year and the 2 years immediately before that, counting:

| All the days in the current year |

| : |

| 1/3 of the days you were present in the first year before the current year, and |

| 1/6 of the days you were present in the second year before the current year. |

Example: Rahul – Substantial Presence Test (SPT) Calculation

Rahul is not a U.S. citizen and does not have a Green Card.

His physical presence:

- 2025 (Current year): 120 days

- 2024 (1st previous year): 120 days

- 2023 (2nd previous year): 120 days

Step 2: Apply SPT Calculation

For SPT:

- All days in current year are counted

- One-third of previous year days are counted

- One-sixth of second previous year are counted

Calculation:

| 2025 |

| 120 days × 100% = 120 days |

| 2024 |

| 120 days × 1/3 = 40 days |

| 2023 |

| 120 days × 1/6 = 20 days |

| Total SPT Days |

| 120 + 40 + 20 = 180 days |

| Final Tax Residency Status |

| Rahul is: |

| Non-Resident Alien (NRA) for U.S. tax purposes |

| Tax Filing Form |

| If Rahul has U.S. taxable income: |

| He generally files Form 1040-NR (U.S. Nonresident Alien Income Tax Return) |

Question

Rahul stayed 120 + 120 + 120 = 360 days over three years. Why is he still a non-resident?

Because SPT does not count all three years equally. The current year is fully counted, the previous year is weighted at one-third, and the second previous year is weighted at one-sixth

Visa Holders and U.S. Tax Residency: Is SPT Required?

A person living in the U.S. does not automatically become a U.S. tax resident. Tax residency depends mainly on:

- Green Card Test, or

- Substantial Presence Test (SPT)

However, certain visa holders receive special treatment where their days of presence in the U.S. are not counted for SPT purposes.

Students, Trainees, Teachers & Researchers (F, J, M, Q Visas)

Certain individuals on these visas may be treated as Non-Resident Aliens (NRA) even though they physically live in the U.S.

Is SPT required?

Yes, SPT is the normal rule.

However, before applying SPT, we check whether the individual qualifies as an Exempt Individual.

If exempt:

- Days of presence are excluded from SPT calculation

- Therefore, they generally remain Non-Resident Aliens

Examples

Student Example (F-1 Visa)

| Rocky comes from India to study in the U.S. on an F-1 visa. |

| He stays: |

| 200 days in 2025 |

| Normally: |

| 200 days may satisfy SPT |

| But: |

| Because he is an eligible F-1 student: |

| His days may not be counted for SPT (during the exempt period) |

| Result: |

| Non-Resident Alien for tax purposes |

Teachers and Researchers (J-1 Visa)

A teacher/researcher on a J visa may also be exempt from counting days for SPT if the conditions are satisfied.

Result:

- SPT calculation is not applied during the exempt period

- Generally treated as Non-Resident Alien

╔══════════════════════════════════════════════╗

Determining U.S. Tax Residency

╚══════════════════════════════════════════════╝

| Step 1: Are you a U.S. Citizen? |

| Yes Resident Alien for tax purposes Worldwide income taxable |

| No → Continue |

| Step 2: Do you have a Green Card? |

| Yes Resident Alien Green Card Test applies |

| No → Continue |

| Step 3: Are you an Exempt Individual? |

| Examples: |

| F Visa → Students |

| J Visa → Teachers / Researchers / Trainees |

| M Visa → Vocational students |

| Q Visa → Cultural exchange participants |

| A Visa → Foreign government employees |

| G Visa → International organization employees |

| Yes |

| Days generally not counted for SPT Generally, Non-Resident Alien (NRA) |

| No → Continue |

| Step 4: Apply Substantial Presence Test (SPT) |

| Check: |

| 31 days in current year, and |

| 183-day formula |

| If satisfied: |

| Resident Alien |

| If not satisfied: |

| Non-Resident Alien |

Very easy to understand sir . Thanks a lot .

Read in detail and get updated…

Very informative. Thank you sir

Thank you!!

Very insightful sir. Thank you.

Happy to get the feedback! Stay tuned.

Very simple to read & understand. Thank You Sir

Good to hear Sumit! Stay tuned..

The practical examples made the concepts easy to grasp. Looking forward to more such insightful blogs, Sir!

Thank you Hrik!!

Your blogs always make complex topics easy to understand.

Sir can you kindly explain spt in details ?

I think if you go through it thoroughly, you will find it helpful.

I truly enjoyed it, sir; your explanation was excellent.

Good to hear!! stay tuned..

This blog is very helpful just like others posted here . Thank u sir for providing all these important concepts and helping us.

Good! keep yourself updated..

Thank you sir for always being so thoughtful and creative.

Thank you!!

Very easily explained sir….easy to understand

Thank you! Stay tuned.