Accrual Basis of accounting is a fundamental accounting assumption for the preparation and presentation of financial statements as per Accounting Standard (AS) 1, disclosure of Accounting Policies. Additionally, Section 128 of the Companies Act,2013 requires maintenance of books of accounts by Companies on the Accrual Basis.

Many businesses prefer to use cash accounting because the financial statements closely reflect their cash position, which is especially important for small-business owners/professions.

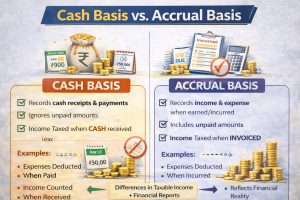

Let’s understand the differences between the two methods of accounting

| Cash Basis | Accrual Basis |

| Revenue recorded when cash is received | Revenue recorded when earned, regardless of payment timing |

| Expenses recorded when cash is paid out | Expenses recorded when incurred, regardless of payment timing |

| Matching principle does not apply | Revenue and expenses are matched to each other in the period the revenue was earned. |

Section 145 provides that income under the head Profits and Gains of Business or Profession shall be computed in accordance with:

- The Cash System, or

- The Mercantile (Accrual) System,

regularly employed by the assessee.

This means the Income-tax Act does not mandate one single system for everyone. The method regularly followed by the taxpayer becomes the starting point

Most companies and manufacturing units follow the mercantile (accrual) system due to the requirements of the Companies Act and Accounting Standards.

Illustration

- Sales made during the year: Rs.10,00,000

(Rs.3,00,000 not yet received) - Expenses incurred: Rs. 6,00,000

(Rs.1,00,000 unpaid)

Under the accrual system:

- Income = Rs.10,00,000

- Expenses = Rs.6,00,000

- Profit = Rs.4,00,000

Even if cash is not fully received or paid, income and expenses are recorded when earned or incurred.

This Rs.4,00,000 becomes the base for computing PGBP, subject to adjustments under the Income-tax Act (such as Sections 43B, 40A (3), depreciation rules and other provisions etc.)

Professional Example – Cash System

Certain professionals such as doctors, consultants, or small practitioners may maintain books under the cash system.

Illustration

- Fees received: Rs.5,00,000

- Fees outstanding: Rs.2,00,000

- Expenses paid: Rs.2,00,000

- Expenses outstanding: Rs.50,000

Under the cash system:

- Income = Rs.5,00,000

- Expenses = Rs.2,00,000

- Profit = Rs.3,00,000

Outstanding income and unpaid expenses are ignored.

This Rs.3,00,000 becomes the base for PGBP computation.

Where the Confusion Arises

Students may mistakenly assume:

PGBP means accrual system.

This is incorrect.

PGBP means:

Profit computed according to the method of accounting regularly employed, subject to the provisions of the Income-tax Act.

- The method of accounting determines when income and expenses are recognised.

- The Income-tax Act determines whether they are allowable or taxable.

Important Conceptual Difference

| Aspect | Business (Accrual) | Small business/Profession (Cash) |

| Method of Accounting | Mercantile | Cash (if regularly followed) |

| Income Recognition | When earned | When received |

| Expense Recognition | When incurred | When paid |

| Tax Adjustments Applicable | Yes | Yes |

Takeaway:

- Business entities generally follow accrual accounting because of statutory requirements.

- Professionals may follow cash accounting or accrual accounting

But in both cases, taxable income under PGBP is determined by:

- Starting from the chosen accounting method and then applying the provisions of the Income-tax Act.

Understanding this distinction removes a major conceptual confusion and strengthens practical clarity for examinations and interviews.