Net Present Value (NPV) and Internal Rate of Return (IRR) are two fundamental tools used to evaluate a project’s profitability.

NPV is an absolute measure of the difference between the present value of cash inflows and the present value of cash outflows over a specific period of time. It considers the time value of money, which means that the same amount received in the future is worth less than the same amount received today due to risk factors, such as uncertainty, volatility, inflation and the opportunity costs of investing the money elsewhere.

IRR is the rate of discount at which the present value of an investment’s cash inflows equals the present value of its cash outflows. It represents the rate of return that makes the NPV of an investment zero. A proposal is accepted only when IRR is higher than the required rate of return (cut-off rate). If it is lower, the proposal is rejected.

In other words, IRR is the maximum rate of interest that could be paid for the capital employed over the life on an investment without loss on the project.

Case study

A Finance Manager of a manufacturing company is preparing a proposal for an expansion project. The company plans to install new machinery that will increase production and generate additional revenue over the next five years.

Before approaching the bank for funding, the Finance Manager meets the General Manager (Finance) to discuss the proposal.

The GM carefully listens and then asks a very practical question:

Before we approach the bank for loan sanction, I want to know whether the project is financially viable. Have you calculated the Net Present Value (NPV) and Internal Rate of Return (IRR) of the project?

The Finance Manager replies:

Yes sir. I have estimated the project cash flows for the next five years considering corporate tax of 30% and depreciation at 20%. Using these figures, I have calculated both NPV and IRR.

The GM then says: Good. If the NPV is positive and the IRR is higher than our cost of capital, the project will be financially sound and we can confidently approach the bank for funding

- Net Present Value (NPV)

- Internal Rate of Return (IRR)

These techniques consider time value of money, which is essential in long-term investment decisions.

Project Information

| Particular | Amount |

| Initial Investment in Plant & Machinery | Rs.10,00,000 |

| Project Life | 5 years |

| Corporate Tax Rate | 30% |

| Depreciation Rate | 20% (WDV method) |

| Expected Annual EBIT | Rs.4,00,000 |

| Cost of Capital | 12% |

Step 1: Depreciation Calculation (20% WDV)

| Year | Opening Value | Depreciation (20%) |

| 1 | 10,00,000 | 2,00,000 |

| 2 | 8,00,000 | 1,60,000 |

| 3 | 6,40,000 | 1,28,000 |

| 4 | 5,12,000 | 1,02,400 |

| 5 | 4,09,600 | 81,920 |

Step 2: Profit After Tax and Cash Flow

EBIT = Rs.4,00,000 every year

Example Year 1 calculation:

EBT

= EBIT – Depreciation

= 4,00,000 – 2,00,000

= 2,00,000

Tax (30%) i.e. 30% of 2,00,000 = 60,000

PAT= 1,40,000

Cash Flow: = PAT + Depreciation

= 1,40,000 + 2,00,000

= 3,40,000

Cash Flow Table

| Year | PAT | Depreciation | Cash Flow |

| 1 | 1,40,000 | 2,00,000 | 3,40,000 |

| 2 | 1,68,000 | 1,60,000 | 3,28,000 |

| 3 | 1,90,400 | 1,28,000 | 3,18,400 |

| 4 | 2,08,320 | 1,02,400 | 3,10,720 |

| 5 | 2,22,656 | 81,920 | 3,04,576 |

Step 3: Net Present Value (NPV)

Discount Rate = 12%

| Year | Cash Flow | PV Factor (12%) | Present Value |

| 1 | 3,40,000 | 0.893 | 3,03,620 |

| 2 | 3,28,000 | 0.797 | 2,61,416 |

| 3 | 3,18,400 | 0.712 | 2,26,701 |

| 4 | 3,10,720 | 0.636 | 1,97,018 |

| 5 | 3,04,576 | 0.567 | 1,72,695 |

Total PV of Cash Inflows

≈ Rs. 11,61,450

Initial Investment

= Rs.10,00,000

NPV:

Since NPV is positive, the project is financially acceptable.

Now we apply IRR calculation.

So, at 12% discount rate → NPV is positive.

This means IRR must be higher than 12%.

Calculate NPV at Higher Discount Rate (20%)

PV factors at 20%

| Year | Cash Flow | PV Factor (20%) | Present Value |

| 1 | 3,40,000 | 0.833 | 2,83,220 |

| 2 | 3,28,000 | 0.694 | 2,27,632 |

| 3 | 3,18,400 | 0.579 | 1,84,354 |

| 4 | 3,10,720 | 0.482 | 1,49,362 |

| 5 | 3,04,576 | 0.402 | 1,22,440 |

Total PV of inflows

≈ Rs.9,67,008

Now, NPV:

So, at 20% discount rate → NPV is negative.

This means IRR lies between 12% and 20%.

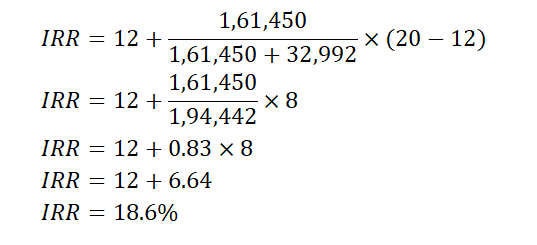

Applying IRR Formula =

Where:

L = Lower discount rate (12%)

H = Higher discount rate (20%)

NPV at 12% = +1,61,450

NPV at 20% = –32,992

Now substituting values:

Final Result

| Method | Result |

| NPV | Rs.1,61,450 |

| IRR | = 18.6% |

| Cost of Capital | 12% |

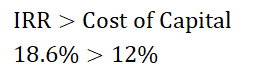

Decision

Since:

✔ Project should be accepted.

Finance Manager’s Interpretation (For Bank Loan)

The finance manager can argue that:

- The project generates strong cash flows

- IRR is significantly higher than borrowing cost

- Loan repayment capacity is financially sound

Therefore, the expansion project is economically viable.