Section 43B of the Income Tax Act provides a list of expenses can be claimed as deductions from business income only in the year of actual payment and not in the year when the liability to pay such expenses is incurred.

Section 40A (3) disallows tax deductions on expenses above Rs. 10,000 made in cash in a single day to a single person.

Under PGBP, certain expenses are disallowed:

- If not paid (Section 43B)

- Disallowed payment in cash beyond prescribed limit (Section 40A(3))

Items Covered under Section 43B

| GST / VAT / Customs Duty |

| Employer’s PF / ESI contribution3 |

| Bonus / Commission to employees |

| Interest to bank / financial institution |

| Leave encashment |

| Allowed only if actually paid (before return filing due date in certain cases). |

Section 40A (3) – Core rule

If payment:

| Exceeds Rs.10,000 per day per person made in cash. Entire expenditure disallowed. |

| (Rs.35,000 limit for transporter) |

Rule 6DD – Major exceptions: There can be practical scenarios where cash payment is not always possible and the above disallowance does not occur when a taxpayer makes payments in certain situations

| Cash payment allowed if made to: |

| Government |

| Bank |

| On bank holiday |

| In areas without banking facility |

| Farmer / cultivator / producer |

| For agricultural or animal products |

Practical Example – Manufacturing Unit

Situation 1: Under Section 43B, following will be disallowed if not paid:

- GST Rs.1,50,000

- Employer PF Rs. 80,000

- Interest to Financial Institution Rs.1,20,000

Total Disallowance = Rs.3,50,000

So, taxable income increases by Rs. 3,50,000

Situation 2:

A factory purchases raw material worth Rs.60,000.

Payment made:

- Rs.60,000 in cash on same day to supplier.

In Books:

Purchase Expense Rs.60,000 is fully recorded and deducted.

In PGBP:

Since cash payment exceeds Rs.10,000, entire Rs. 60,000 is disallowed under Section 40A (3).

So taxable income increases by Rs.60,000.

Combined Illustration

Book Profit = Rs.10,00,000

Add back:

- Section 43B disallowance = Rs.3,50,000

- Section 40A (3) cash payment = Rs.60,000

Taxable Business Income = Rs.14,10,000

Summary Chart – Section 43B, 40A (3) & Rule 6DD (PGBP Adjustments)

| Particulars | Section 43B | Section 40A(3) | Rule 6DD (Exception to 40A (3)) |

| Nature of Provision | Payment-based allowance | Cash payment restriction | Exceptions where cash payment allowed |

| Objective | Ensure statutory dues are actually paid | Discourage large cash transactions | Protect genuine business needs |

| Trigger condition | Expense accrued but not paid | Payment exceeding Rs.10,000 in cash (Rs.35,000 for transporter) | Cash payment under specified circumstances |

| Treatment in books | Allowed on accrual basis | Allowed if genuine | Allowed if genuine |

| Treatment under PGBP | Disallowed if not paid (allowed on actual payment basis) | Entire expense disallowed | Expense allowed despite cash payment |

| Type of difference | Usually, temporary difference | Permanent disallowance | No disallowance |

| Relevant sections | 43B | 40A (3), 40A(3A) | Rule 6DD |

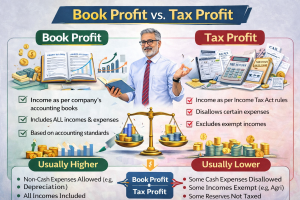

Two profits are different because they are governed by different provisions — Book Profit is prepared as per Accounting Standards and Companies Act, whereas Tax Profit (PGBP) is computed as per Income-tax Act provisions.

Tax liability is calculated on which profit?

Answer: Tax liability is calculated on Taxable Income (PGBP), not on Book Profit.

Assume corporate tax rate = 25%

Tax = 14,10,000 × 25%

= Rs.3,52,500

(Plus surcharge/cess if applicable)

But what about accounting?

In books, profit is Rs.10,00,000.

But tax is calculated on Rs.14,10,000.

So, difference = Rs.4,10,000

Now you can ask:

Is this difference permanent or temporary?

Analysis of the difference

Section 43B (Rs.3,50,000)

If paid next year → deduction allowed later.

This is Temporary difference.

Section 40A (3) (Rs.60,000)

Permanent disallowance.

This is Permanent Difference

Accounting Treatment – DTA & DTL (As per Ind AS 12 / AS 22)

Temporary Difference → Deferred Tax

Temporary difference = Rs.3,50,000

Deferred Tax = 3,50,000 × 25%

= Rs.87,500

Since expense will be allowed in future → creates Deferred Tax Asset (DTA)

Journal Entry for DTA

Deferred Tax Asset A/c Dr Rs.87,500

To Income Tax Expense A/c Rs. 87,500

Total Tax Expense in P&L

| Component | Amount |

| Current Tax (on 14,10,000) | 3,52,500 |

| Less: Deferred Tax Credit | (87,500) |

| Net Tax Expense in P&L | 2,65,000 |

Although company pays tax on Rs.14,10,000, P&L reflects tax considering future adjustment.

- Tax is paid on taxable income.

- But financial statements reflect tax on accounting profit — adjusted through Deferred Tax.

Question:

If statutory audit happens before tax audit, how is DTA/DTL reflected in Balance Sheet?

Answer:

Deferred Tax is not dependent on completion of tax audit.

It is computed:

- Based on Income-tax provisions

- Using management’s computation of taxable income

- During finalisation of accounts itself

Tax audit is only a reporting mechanism under Income-tax Act.

Deferred tax is an accounting requirement under AS 22 / Ind AS 12.

FLOW CHART – From Book Profit to DTA/DTL Recognition

Step 1:

Prepare Financial Statements (Books)

↓

Book Profit as per Companies Act / Accounting Standards

↓

Identify Differences between:

Accounting Profit vs Taxable Profit

↓

Classify Differences:

→ Permanent Differences

→ Temporary Differences

↓

Compute Taxable Income (PGBP)

↓

Calculate Current Tax Liability

↓

Compute Deferred Tax on Temporary Differences

↓

Pass Accounting Entries:

Current Tax Expense

To Deferred Tax Liability (DTL)

Or

Deferred Tax Assets (DTA)

To Current Tax Expense

↓

Final P&L shows:

Current Tax ± Deferred Tax

↓

Balance Sheet shows:

DTA (Non-Current Asset) OR

DTL (Non-Current Liability)

↓

Later:

Tax Audit verifies computation

“Great Explanation! I liked how simply the topic is explained in such easy and simple words. It helped me understand things much better. Thank you so much Sir for sharing such useful content. Looking forward to reading more blogs like this.”