Why do investors buy shares of a company?

Ans:

- For dividend

- For capital appreciation

- For profit

What determines whether a company is valuable or not?

Ans: The value of a firm is determined by its ability to generate future earnings and cash flows.

A firm is financed by:

- Equity shareholders

- Debt holders

So naturally,

Value of the Firm (Market Value Concept)

Value of the firm = Market value of Equity + Market value of Debt

V=S+D

Where:

S=No. of equity shares × Market Price per Share

D=No. of debentures × Market Price per Debenture

So,

Why Market Value (Not Book Value)?

In finance theory (especially capital structure decisions):

- We use market values

- Because they reflect investors’ expectations

- They capture risk and return perception

- They are relevant for shareholder wealth maximization

Suppose:

- 1,00,000 shares

- MPS = Rs. 50

- 10,000 debentures

- Market price per debenture = Rs. 95

Then:

Market value of equity = 1,00,000 × 50 = Rs. 50,00,000

Market value of debt = 10,000 × 95 = Rs. 9,50,000

Value of Firm+ Rs. 59,50,000

All capital structure theories use market values:

- NI Approach

- NOI Approach

- MM Hypothesis

- Trade-off Theory

Under Net Income (NI) Approach

- More debt → Increases value of firm

- WACC decreases

- Ko =( D/V)kd + (S/V)Ke v= total value of firm

S= value of equity

D= value of debt

Under Net Operating Income (NOI) Approach (MM without tax)

- Value of firm is constant

- Capital structure irrelevant

V= EBIT/Ko

- The value of equity S is found as S = V-D

- Ke = EBIT-I/S

Under MM with Tax

Where:

= Levered firm value

= Unlevered firm value

= Tax shield value

What Trade-Off Theory Says

Trade-Off Theory accepts MM tax shield but adds:

- Expected bankruptcy cost

- Financial distress cost

- Agency cost of debt

So the equation becomes:

Now:

- Initially value increases (tax benefit dominates)

- After some point value decreases (distress dominates)

Under:

- Net Income (NI) Approach → Value changes with leverage

- Net Operating Income (NOI) Approach → Total value remains constant

- MM without tax → Capital structure irrelevant

- MM with tax → Value increases with debt (due to tax shield)

Let us take go trough this comparative table

- NI Approach

- NOI Approach

- MM Approach (without tax)

- MM Approach (with tax)

- Trade -Off theory—- in a comparative table format.

Comparative Table

| Theory | Optimal Structure? | Reason |

| NI | 100% Debt | Debt cheaper |

| NOI | Irrelevant | Market adjusts |

| MM (No Tax) | Irrelevant | Arbitrage |

| MM (With Tax) | 100% Debt | Tax shield |

| Trade-Off | Yes | Balance benefit & cost |

Let us take one common numerical example and compute

Assume

EBIT = Rs. 2,00,000

Total Capital = Rs. 10,00,000

Debt = Rs. 4,00,000

Equity = Rs. 6,00,000

Interest Rate = 10%

Cost of Equity (unlevered) = 12%

Overall Cost of Capital (Ko under NOI/MM) = 12%

Interest = 10% of 4,00,000 = Rs. 40,000

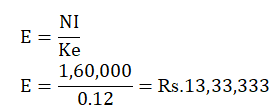

EBT = 2,00,000 – 40,000 = Rs. 1,60,000

Net Income (NI) Approach

Assumptions:

- Cost of equity constant

- Cost of debt constant

- WACC declines with leverage

Step 1: Value of Equity

Step 2: Value of Firm

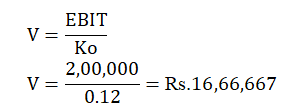

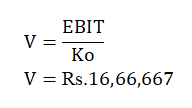

Net Operating Income (NOI) Approach

Assumptions:

- Overall cost (Ko) constant

- Market capitalizes EBIT

- Value independent of capital structure

Value of Equity:

MM (without tax) gives same result as NOI:

Hence,

Equity Value = Rs. 12,66,667

MM with Corporate Tax

EBIT = Rs. 2,00,000

Debt = Rs. 4,00,000

Interest Rate = 10% → Interest = Rs. 40,000

Tax Rate = 40%

Unlevered Cost of Capital (Ko) = 12%

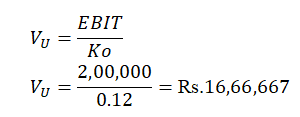

Step 1: Value of Firm under MM (Without Tax)

This is value of firm if no debt.

Step 2: Tax Shield Value

Under MM with tax:

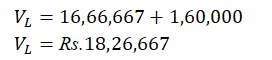

Step 3: Levered Firm Value

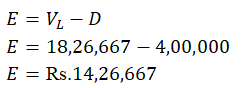

Step 4: Value of Equity

Complete Comparative Table

| Particulars | NI | NOI | MM (No Tax) | MM (With Tax) |

| EBIT | 2,00,000 | 2,00,000 | 2,00,000 | 2,00,000 |

| Interest | 40,000 | 40,000 | 40,000 | 40,000 |

| Tax Rate | 0 | 0 | 0 | 40% |

| Value of Firm | 17,33,333 | 16,66,667 | 16,66,667 | 18,26,667 |

| Behaviour | Value ↑ with Debt | Constant | Constant | Value ↑ due to tax shield |

Why doesn’t Big Company operate with 90% debt?

Ans: Because of

- Credit rating risk

- Bankruptcy risk

- Loss of control

- Agency problems

That is Trade-Off Theory in action and Trade-Off Theory leads to an Optimum Capital Structure.