The bell had just rung, but Mohit and Mrinmoy were still seated, flipping through their notes. The topic for the day was Direct Tax Compliance, and both of them looked slightly unsettled.

Mohit leaned towards Mrinmoy and whispered: I understand income tax theory, but in a manufacturing company interview, they won’t ask definitions. They’ll ask what we actually do for TDS and TCS.

Mrinmoy: Same here. They don’t ask theory. They ask what we actually do in accounts. Vendor payments, job work, transporters, scrap sales… everything is mixed up. I’m not sure who deducts tax, who collects tax, and when.

At that moment, the Professor, who was about to start one topic, noticed their discussion.

Mohit stood up and said:

Sir, from a manufacturing organization’s perspective, we want to clearly understand:

- Where TDS applies,

- Where TCS applies,

- What compliance is expected from an accountant, so that we can confidently answer in interviews

Mrinmoy added: yes Sir, especially what kind of questions can be asked during placement interviews related to TDS and TCS.

He picked up a marker and wrote on the board: Manufacturing Company = Vendors + Labour + Services + Sales

The Professor explained: From the company’s side:

- When you pay, you think of TDS.

- When you receive, you think of TCS

Today, we will discuss TDS and TCS exactly the way an account executive or tax officer in a manufacturing company would handle it —

A Limited Company must deduct TDS when making specified payments such as:

| Section | Nature of Payment |

| 192 | Salary |

| 194C | Contractor |

| 194J | Professional Fees |

| 194I | Rent |

| 194H | Commission |

| 194A | Interest (other than securities) |

| 194Q | Purchase of goods (subject to turnover limit) |

Mrinmoy quickly noted and said: so Sir, interviewers expect us to identify which section applies?”

Professor: Exactly.

Time of Deduction

TDS must be deducted:

At the time of credit OR payment, whichever is earlier.

Time Limit for Deposit of TDS

| Month of deduction | Due date for deposit |

| April – February | 7th of next month |

| March | 30th April |

If you say only ‘payment’ in interview — you lose marks.

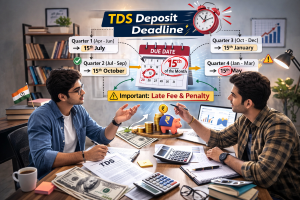

Quarterly TDS Return Filing

| Quarter | Period | Due Date | Form |

| Q1 | Apr–Jun | 31 July | 24Q / 26Q |

| Q2 | Jul–Sep | 31 Oct | 24Q / 26Q |

| Q3 | Oct–Dec | 31 Jan | 24Q / 26Q |

| Q4 | Jan–Mar | 31 May | 24Q / 26Q |

Forms: There are various types of forms for different types of TDS payments. It includes form 24Q, 26Q, 26QB, 26QC, 27Q and 27EQ.

- 24Q – Salary

- 26Q – Non-salary payments

- And others.

Professor: A manufacturing company is judged by profit and also by compliance.

He summarized:

- Monthly deposit by 7th

- Quarterly returns

- Issuance of Form 16 / 16A

- Reconciliation with books and 26AS

Professor: In a company, compliance is incomplete without entries.

Journal entries – TDS (Limited Company Books)

Example: Professional Fee Rs.1,00,000 (TDS @10%)

At the Time of Booking Expense

Professional Fees A/c…….Dr 1,00,000

To Vendor A/c…………….90,000

To TDS Payable A/c…………10,000

At the Time of Payment to Vendor

Vendor A/c…………….Dr 90,000

To Bank A/c………………90,000

At the Time of Deposit of TDS

TDS Payable A/c………..Dr 10,000

To Bank A/c………………10,000

Professor said now you understand TCS (Tax Collected at Source).

When is TCS Applicable?

Company must collect TCS in cases such as:

| Section | Nature |

| 206C(1H) | Sale of goods (if turnover > Rs10 crore) |

| 206C(1F) | Motor vehicle sale > Rs.10 lakh |

| 206C(1) | Scrap, timber, tendu leaves etc. |

Time of Collection

TCS is collected:

At the time of receipt of consideration.

Due Date for Deposit

7th of next month.

For March – 7th Apri

TCS Return Filing

Form 27EQ (Quarterly)

| Quarter | Due date |

| Q1 | 15 July |

| Q2 | 15 Oct |

| Q3 | 15 Jan |

| Q4 | 15 May |

Professor then said: Let’s see how to pass Journal entries for TCS.

Example: Sale Rs.50,00,000, TCS @0.1%)

At Time of Sale

Debtor A/c…………….Dr 50,05,000

To Sales A/c…………….50,00,000

To TCS Payable A/c…………5,000

At Time of Receipt

Bank A/c………………Dr 50,05,000

To Debtor A/c…………….50,05,000

At Time of Deposit

TCS Payable A/c………..Dr 5,000

To Bank A/c………………5,000

Mohit asked: liability of the deductor is very important.

Professor replied: Correct

If company fails to:

- Deduct TDS

- Deposit TDS

- File return

- Issue certificate

It becomes:

- Assessee-in-default

- Liable for interest

- Liable for penalty

- Liable for prosecution in serious cases

*Directors may also face consequences in extreme cases.

Professor then said: look at this practical compliance flow in Limited Company

- Identify nature of payment

- Verify PAN

- Deduct correct rate

- Deposit within due date

- File quarterly return

- Issue TDS certificate

- Reconcile with Form 26AS

As a Finance Executive you must ensure

✔ Vendor master verification

✔ Threshold monitoring

✔ Monthly TDS working sheet

✔ Reconciliation with books

✔ Challan matchingConclusion: Students, remember — this article is not exhaustive. It is only a synoptic view designed to help you confidently face interview questions in a manufacturing organization.

For detailed understanding, you must always refer directly to the relevant provisions of the Income-tax Act, especially Sections 192, 194C, 194J, 194I, 194Q, 201 and 206C.

It helped me a lot to understand the real concept behind TDS/TCS

Thanks a lot sir for such an insightful blog .